How should organic products be sold? In health food stores, food retailers or even discounters – there are many points of view and interests. The pioneers who built everything are worried about their well-deserved success. However, they also see an urgent need to increase the proportion of organic food in our diet so that agricultural land is also cultivated according to organic guidelines wherever possible. Of course, this is only possible if the entire trade is included. The milk price also plays a central role in this debate, as it often serves as an indicator of the value of organic farming.

So it is no wonder that there is currently a heated debate – particularly with regard to Demeter and Bioland at Kaufland and Lidl. In this discussion, however, one aspect is neglected: there is a world of difference between an association making its label available to a retailer’s own brand and providing the owner of this own brand with all marketing instruments, including pricing. Or whether an association like Demeter allows producers who have the Demeter logo on their products to sell them in channels like Kaufland. The milk price in particular shows how big the differences are in the various distribution channels and what challenges this poses for organic farmers.

Even though vertical price fixing has long since been abolished, brands still have an influence on the conditions under which they are sold. In the case of private labels, however, the respective retailer decides completely autonomously. This also applies to the pricing of sensitive products such as milk, whose value chain is particularly closely linked to ecological standards and the livelihoods of farmers.

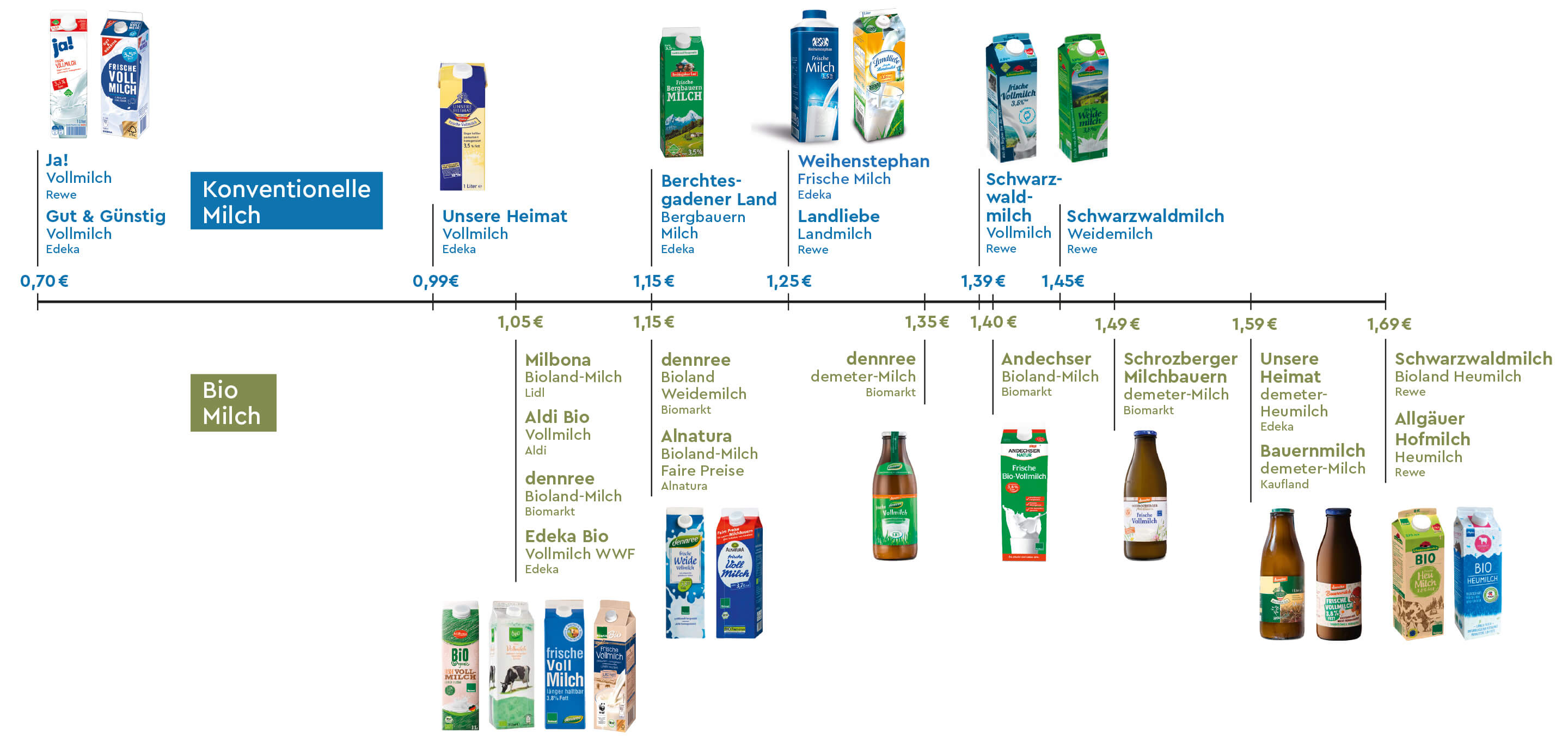

The example of fresh milk can be used to analyze how the new structure is already having an impact. How real added value has a direct influence on the milk price and the value of a product. And how the positioning of individual products can cancel this out.

Fresh milk in particular is a good example because factors such as differences in taste and recipes do not have a major influence on the products and they are therefore easy to compare.

Real added value leads to real “more value” – this is particularly evident in our milk example: whole milk in combination with Demeter, glass bottles beat tetra packs, pasture, fair prices, but also strong brands (these are also sometimes more expensive in the conventional sector than organic without a brand) are further factors. And then there are also prizes that are made politically.

Our chart shows Rewe at the upper end of the price scale, much more expensive than all the others. At the lower end, on the other hand, are private labels, including those with the Bioland label. With the fatal consequence that Bioland can no longer reflect the added value that the brand actually has in the milk price. The price increase can be seen not only at Lidl, but now also in Denree’s own brands.

This is an observation of the price situation – not a valuation. The fact is: There are now so many farms converting to Bioland that many dairies no longer accept organic farmers. What then? Label all products with Bioland and market them as entry-level prices? Or does Bioland then run the risk of gambling away its brand strength because it must be assumed that discounters such as Lidl will always position a private label product – in this case Bioland milk – against Aldi & Co at the entry-level price?

It remains exciting. But one thing we can learn here is that the only thing that really helps in the long term is genuine added value, a strong brand and a milk price that fairly reflects the value chain.

back

back