The Corporate Sustainability Directive (CSRD for short) is the further development of the previously applicable EU-wide Non-Financial Reporting Directive (NFRD) and aims to expand and standardize sustainability reporting throughout the EU. The scope and extent of the directive now puts sustainability reporting on a par with financial reporting.

The CSRD will place significantly more companies under obligation than the EU-wide NFRD and the national CSR-RUG have done to date. According to estimates, there will be around 15,000 companies.

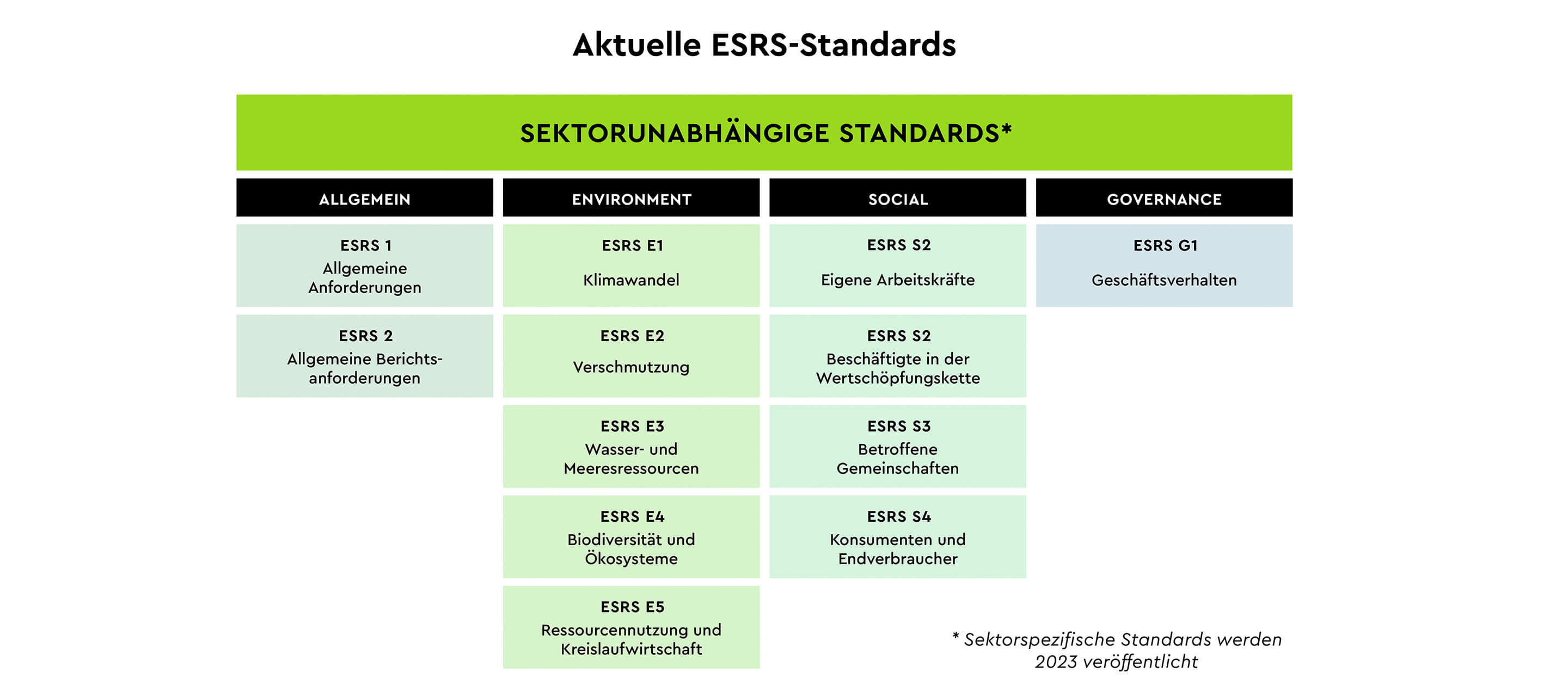

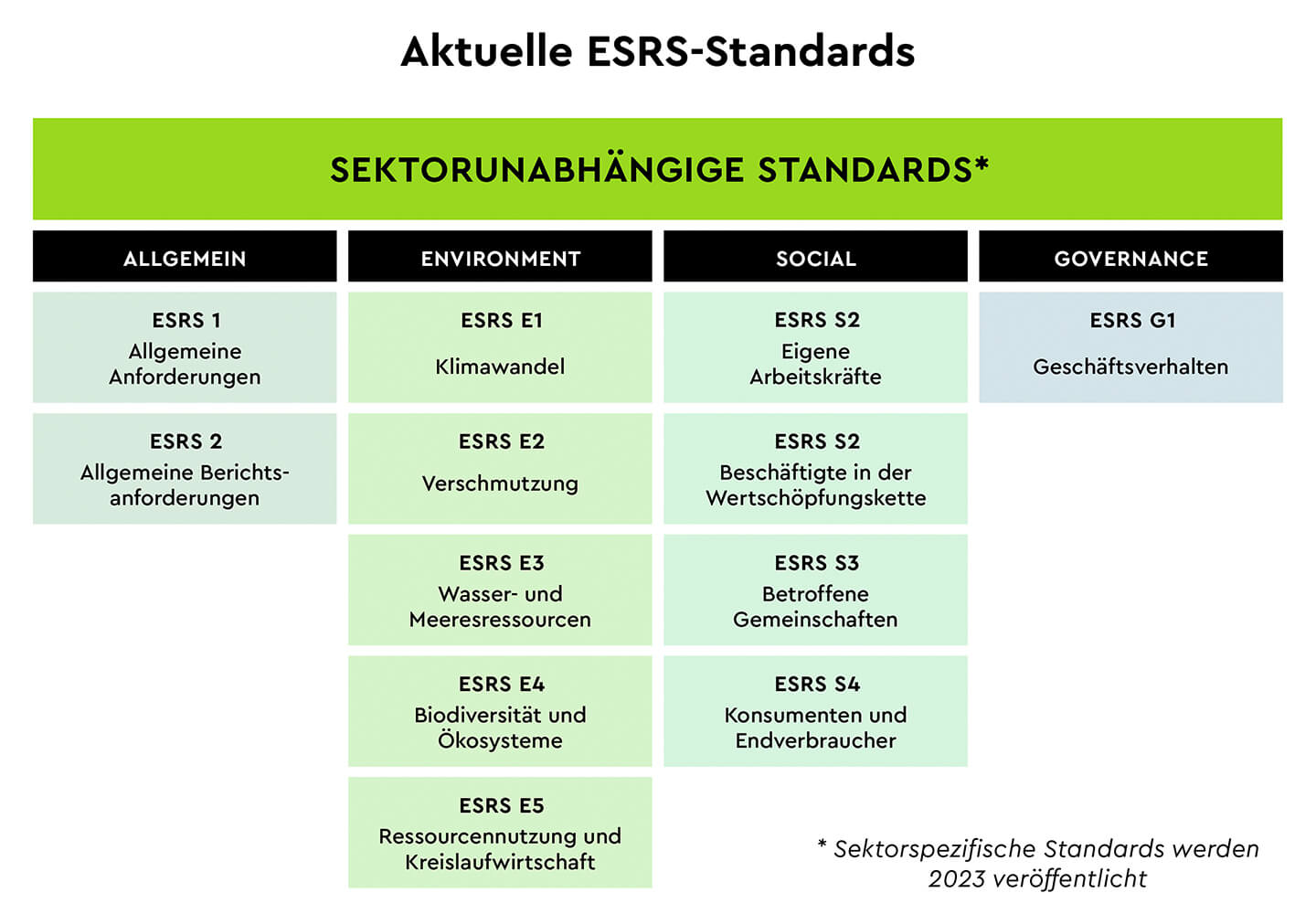

The CSRD provides for a uniform, Europe-wide reporting standard, the European Sustainabiliy Reporting Standard (ESRS), which is intended to make reporting more transparent, consistent and comparable. The ESRS is based on the two standards of the Global Reporting Initiative (GRI) and the Sustainability Accounting Standards Board (SASB) and specifies a selection of topics that should be reported on if the topic is material for the company.

NEW (November 2023):

At the end of October, EFRAG published an initial version of an Excel list with all the data points of the new European reporting standard (ESRS), which lists the specific figures and data by topic area. The list therefore provides an initial orientation as to which data is to be reported voluntarily or mandatorily and in what form.

The list contains 1,170 data points, which must be specified either quantitatively or descriptively. As this is initially a draft, adjustments can still be made. The list is available

here

for download.

The CSRD anchors the so-called “double materiality” in reporting and thus specifies the selection of topics to be reported. Companies are now obliged to report not only on the effects that the company has on people and the environment (inside-out perspective) but also on the effects that people and the environment have on the company (outside-in perspective). Previously, a topic only had to be reported on if both materiality aspects applied. The topics are evaluated from both perspectives by analyzing certain characteristics and visualized in a materiality matrix.

CSRD reporting provides for the publication of all sustainability information in a machine-readable format in a Europe-wide database, which is still at the planning stage, and according to a predefined structure. Readers and technical systems should be able to find information more quickly.

In addition, companies that are required to publish an annual report are also obliged to publish all sustainability information in a separate section of the management report.

As part of the annual reporting, sustainability reporting is also subject to audit – but initially only with limited assurance. However, an extension to a mandatory reasonable assurance test is certainly possible.

Sustainability is becoming an obligation for more companies – and that’s a good thing. However, this does not make sustainability the core value of all these brands and companies. There is therefore still real potential for brands that have been operating sustainably from the outset to differentiate themselves, which can be used in a targeted manner in communications.

However, for companies that are only now increasingly addressing the issue of sustainability, the CSR reporting obligation also offers the opportunity to integrate sustainability into brand, product and HR communication.

Sustainability continues to be a relevant factor for consumers, retailers, investors and potential employees.

back

back